Machine Learning

FastAPI

Streamlit

MLOps

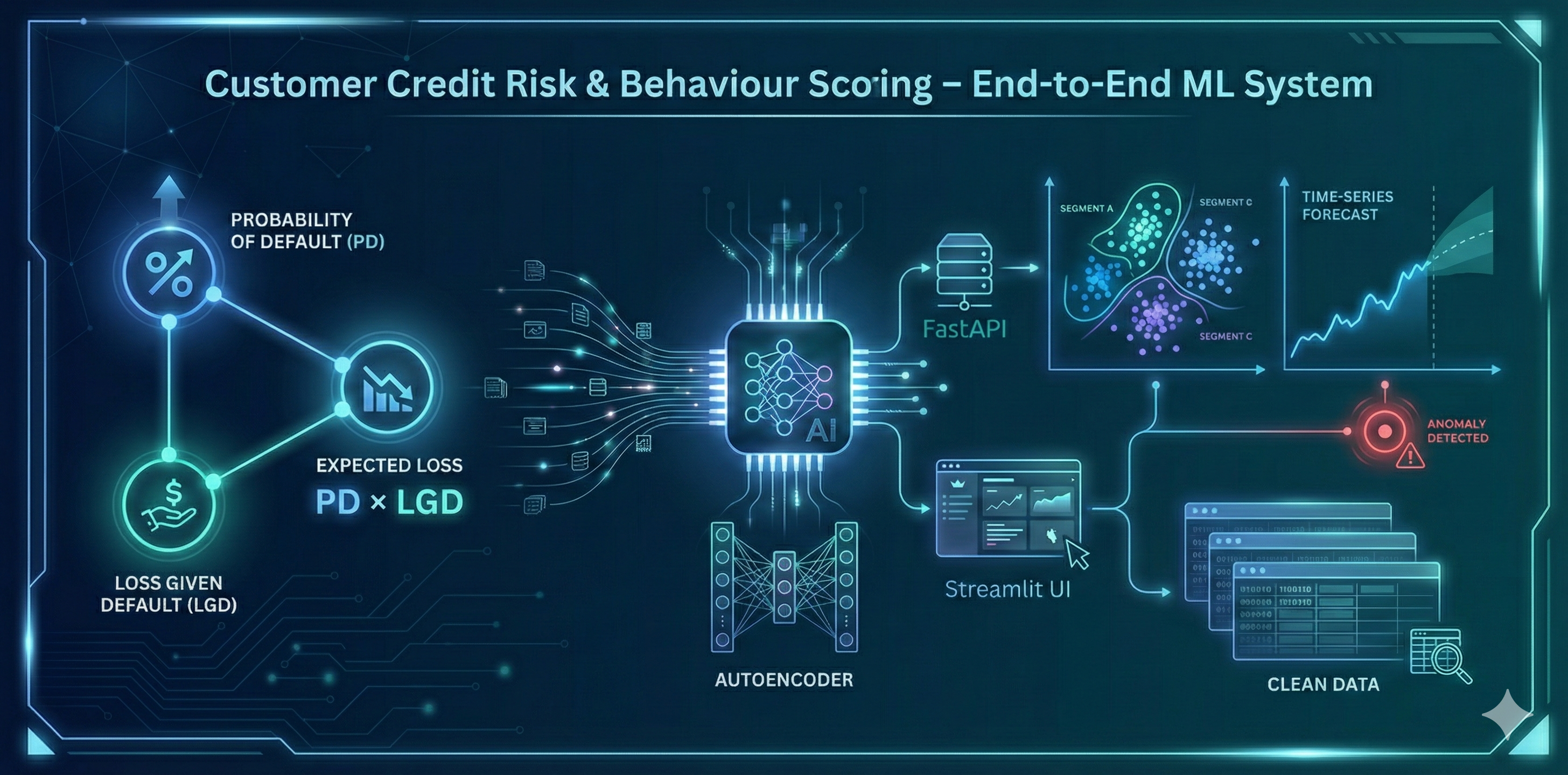

A full end-to-end machine learning system for credit risk modeling that predicts:

- Probability of Default (PD) using XGBoost

- Loss Given Default (LGD) using LightGBM

- Expected Loss (PD × LGD)

- Customer Segmentation using KMeans

- Behavioural Anomaly Detection using Isolation Forest

- Autoencoder embeddings for deep behavioural representation

- Default-rate time-series forecasting with ARIMA

The project includes a complete data → model → deployment pipeline with a FastAPI microservice for real-time scoring and a Streamlit dashboard with human-friendly inputs, tooltips, and live predictions.

System Architecture

- DuckDB for fast SQL-based feature engineering

- XGBoost & LightGBM for PD/LGD modeling

- PyTorch Autoencoder for behavioural embeddings

- statsmodels for ARIMA forecasting

- FastAPI REST service with model caching

- Dockerized backend for reproducible deployment

- Streamlit UI for scoring and visualizations

This project showcases full-stack ML engineering: data cleaning, feature pipelines, supervised + unsupervised models, deep learning, microservice deployment, dashboarding, and documentation.

Tech Stack

Python, DuckDB, XGBoost, LightGBM, PyTorch, scikit-learn, statsmodels, FastAPI, Streamlit, Docker.